New Allocation Guidelines for MD Districts

When the Blueprint for Maryland's Future legislation passed in 2021, sweeping funding and policy reforms to improve the quality of the public education system in the state became law. This landmark piece of legislation aims to improve the state’s investment in and operation of its public school system. The Blueprint was based on recommendations made by the Commission on Innovation and Excellence in Education (commonly known as the Kirwan Commission).

A portion of the Blueprint is focused on equitable increases in funding by student, school, and county to improve upon Maryland’s current funding system. In particular, the legislation introduces new requirements for how districts construct their resource allocation models—the set of guidelines or rules that define how resources flow to schools.

Under the new “75% rule,” districts must observe a new floor on dollars attributed to schools in specific categories. This rule applies to both state and local aid. While there are five policy areas the commission plans to address, the allocation categories break down to:

- Foundation program

- Compensatory program

- English Learner program

- Special Education program

- Public providers of prekindergarten

- College and career readiness

- Comparable wage index adjustments

- Transitional Supplemental Instruction

Additionally, dollars provided due to concentration of poverty must be spent 100% at the school-level.

This new guideline means that districts must demonstrate that 75% of their dollars within each category are flowing to school sites. (That’s a lot of school-level attribution!) This requirement is intended to ensure that site-level resource distribution reflects the way dollars are distributed to the district by the state. To put it conversationally, it’s as if the state of Maryland has said, “We’ve distributed funds based on the number of students you enroll with specific characteristics. Therefore, these categories of dollars should end up at the schools where these students are located.”

The Attributable Expenses Complication

No matter how a district determines its staffing or dollar resource allocations to school sites, districts must be able to demonstrate that enough dollars are planned at each school site to meet the 75% requirement in each of the eight Blueprint allocation categories. However, resources that primarily benefit students at school sites are often recorded in central office account locations for budgeting (and even sometimes for actual expenditures). Expenses are planned and recorded in central office departments because they are managed there—but in many cases, the funding isn’t actually being spent there. In other words, many districts run their accounting systems based on control, not impact.

For example, the district head of pupil support services may record all social workers in their department. This person is directly responsible for hiring and managing social workers as well as setting their caseloads. Despite the fact that a central office director determines how many social workers are required and in what schools, the social workers themselves are assigned to school sites and work directly with students. The impact and investment is directly in school sites, but the control is in the central office.

Another common example of expenses that may be recorded in the central office instead of school sites are benefits. Benefits may be budgeted for centrally, because they are centrally negotiated, managed, and estimated, but of course those resources are being spent on staff at school sites.

Centrally-managed funds may appear to be noncompliant with the new regulations introduced through the Blueprint because they are not identified at the school site to count toward the 75% threshold.

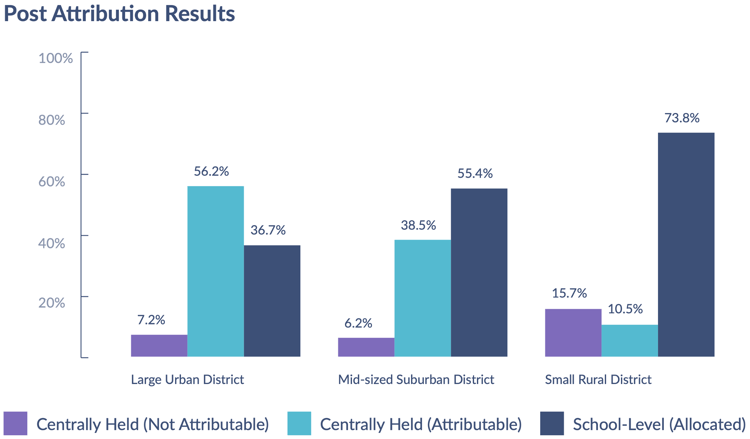

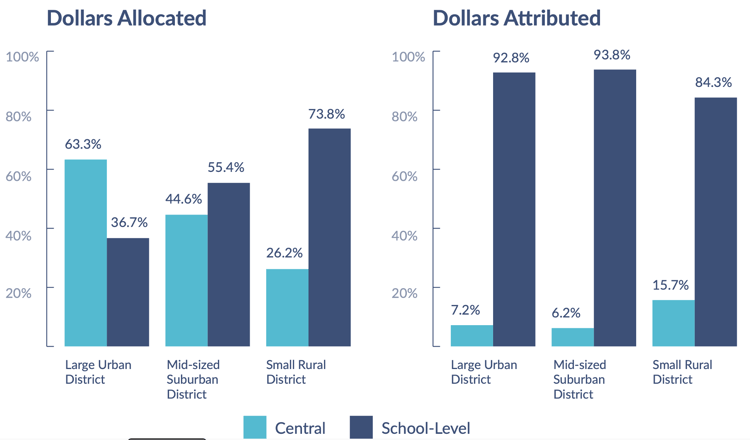

Across the country, the percentage of dollars that sit in central offices versus school sites differs widely. The graph below illustrates this concept with a sample of ten districts. The bars represent actual expenses based on the central versus school-level classifications in each district’s chart of accounts.

Although the account codes specify “central” or “school,” in reality, there are actually three types of expenses at play:

- School-Level: School-level expenses reported at school-sites

- Centrally Held (Attributable): Money that is centrally held, but attributable to school-sites. Examples include utility bills, benefits, student services cost center that serves multiple school sites, etc.

- Centrally Held (Not Attributable): Central expenses reported to central office

In these examples, when central expenditures are appropriately allocated to school sites, a large portion of dollars are shifted to schools. This represents a shift of attributing centrally-controlled expenditures to the school sites where those expenditures benefit students.

This attributable expenses problem is a huge challenge for showing that your district has actually spent 75% of funds at school sites. At first glance, your district may appear to fall short of the 75% if dollars are managed and processed centrally. This attribution challenge is a reporting process challenge. The key question to consider is: how do we define central services versus school-based allocations? Is this distinct for budget versus expenditures?

Resource Allocation Models to the Rescue

Where can districts start to attribute appropriate central office expenses to school sites? What can make this work easier? Resource allocation models are an ideal place to begin. The rules that govern how dollars are allocated to schools is the single most important lever in a district for advancing resource equity or perpetuating inequity. What’s more, a passive approach to equity guarantees inequity—this is the spirit of the Blueprint legislation. (For more on these concepts, check out our eBook, Better than Equal: Building Equitable Resource Allocation Models.)

Resource allocation rules can help achieve two distinct types of equity:

- Horizontal equity is the “equal treatment of equals” in resource distribution. By using a series of well-defined rules, schools that have the same characteristics are set to receive the same funding. By maximizing the dollars allocated through rules and not exceptions, horizontal equity is improved.

- Vertical equity is the differential treatment of different groups in resource distribution. By using rules that consider student need characteristics, school resources adjust to meet the needs of students. Vertical equity is harder to achieve because answering “how much difference in resource needs exists between these two students?” is both an empirical and policy-level question.

Having a rigid set of rule-based allocations is key to demonstrating compliance with the new 75% rule under the Maryland Blueprint. The critical task is to define the set of rules that determine exactly how dollars or staff are assigned to each school site. When your district has a methodology for how dollars are assigned to school sites, it can clearly tie those dollars back to the revenue source—including both state and local funds. Then, your district can group the rules by Blueprint category, assign the dollar amounts to school sites according to each rule, and thereby demonstrate compliance with the requirement to attribute 75% of funds to school sites by category.

For some districts, defining a resource allocation model is simply about finding a new way to present the practices that already exist to determine allocations. Whether or not your district uses the term “resource allocation model,” you likely already have practices that generate allocations and serve as a model for how resources are allocated to schools, such as:

- How special education programs are staffed

- Rules that govern janitorial staffing, utilities, and capital expenditures from operations

- Guidelines from union contracts that determine class sizes and teacher to student ratios

Framing these practices as rules within a formula creates a defined framework for how dollars flow from state and local revenue sources to districts and then out to school sites. For district administrators, the challenge lies in collecting the many models that already exist and creating one summary to describe how dollars are flowing. The rules need to be understandable, clear, and written in one place. Not only will this exercise make complying with the Blueprint’s 75% rule easier, it also affords your district the ability to adapt your allocation plans as revenue and enrollment projections are finalized.

The example below shows an excerpt of a resource allocation model where the per-pupil and by-school amounts are clearly summarized with a descriptive narrative. A rules-based model like the snapshot shown below is a useful tool for showing Blueprint-defined allocation categories down to the school-site. This model and the report shown below were created in Allovue Allocate.

Meeting the 75% Rule

Step 1: Revenue

Determine revenue per school from each of the “unrestricted” fund pots.

Step 2: Allocation Rules

Group resource allocation rules by Blueprint category. Then, ensure that rules target the Blueprint’s specified student groups and allocate staff and money for stated purposes.

Step 3: Review

Demonstrate that the total allocation by Blueprint category meets the 75% value across the district and ensure that school-by-school rule group allocations are allocated correctly. Adjust rules and groupings iteratively.

Remember: The work doesn’t stop here. Districts must also grapple with how to get from allocations to plans to actions. How can districts move beyond refining inputs to their resource allocation model and ensure that adjustments are reflected in budget plans? Instead of separating budget line items into complex program codes, consider structuring a budget plan around strategies that align to the priorities outlined in the Blueprint and legislation. Showing the alignment of programs and activities to goals is a powerful tool for transparency and accountability.

For more information on The Blueprint for Maryland's Future and specific requirements for K-12 districts, visit the Maryland State Department of Education website. To learn more about Allovue's resource allocation model tool, visit our resource equity solutions page.

ABOUT THE AUTHOR

Allovue works with districts and state departments of education across the country to allocate, budget, and manage spending. Allovue's software suite integrates seamlessly with existing accounting systems to make sure every dollar works for every student. Allovue also provides additional services such as chart of accounts and funding formula revisions.